Introduction: What Is EV Insurance?

EV insurance is no longer a niche financial product quietly sitting on the sidelines of the auto industry. It has evolved into a specialized safety net designed for vehicles that think, charge, and move very differently from traditional cars. At its core, it protects electric vehicles against damage, loss, and liability, but the logic behind it goes far beyond standard motor coverage. Electric cars rely on high-voltage batteries, software-driven systems, and charging infrastructure that demand a more tailored approach to risk.

What sets this coverage apart is the way insurers evaluate value and vulnerability. A battery pack alone can account for a large portion of an EV’s cost, and its performance degrades differently than an engine. That technical reality forces insurers to rethink how protection is structured, priced, and serviced, making EV insurance a distinct category rather than a rebranded version of old policies.

The surge in electric vehicle adoption has pushed this shift into the spotlight. In 2025, governments, manufacturers, and consumers are aligned around electrification, and insurance has had to keep pace. As more drivers switch to EVs for environmental, economic, or technological reasons, the demand for coverage that actually understands these vehicles has grown from optional to essential.

What Does EV Insurance Cover?

EV insurance coverage is built around the components that make electric vehicles unique, not just the fact that they are cars. Instead of focusing solely on body damage and liability, these policies dig deeper into the systems that power and control the vehicle. This expanded scope ensures that the most expensive and sensitive parts of an EV are not left exposed.

Battery coverage

The battery is the financial and functional heart of an electric vehicle. Electric vehicle insurance typically protects against damage caused by accidents, electrical faults, or environmental factors, recognizing that battery replacement costs can be significant.

Electric motor and charging equipment

Electric drivetrains operate differently from combustion engines. Coverage often extends to motors, inverters, and even home charging equipment when damage is linked to insured events under EV insurance.

Fire, theft, and accident coverage

High-voltage systems introduce unique fire risks, while EVs remain attractive theft targets. Comprehensive protection handles these threats without treating them as edge cases.

Roadside assistance for EVs

Running out of charge is not the same as running out of fuel. Many electric vehicle insurance policies include EV-specific roadside support, including towing to the nearest charging station.

Is EV Insurance Mandatory?

EV insurance is shaped by the same legal frameworks that govern all vehicles, but its application carries extra nuance. In most regions, liability coverage is mandatory for any car that uses public roads, regardless of how it is powered. Electric vehicles are no exception to that rule, even though their mechanics differ.

The real distinction appears when drivers move beyond basic legal compliance. Third-party coverage satisfies the law by protecting others from damage or injury caused by the EV, but it does little to safeguard the vehicle itself. Comprehensive EV insurance steps into that gap, addressing the higher repair costs and specialized parts that define electric mobility.

As governments push EV adoption, some markets are introducing incentives or regulatory tweaks that indirectly encourage broader coverage. This makes comprehensive protection less of a luxury and more of a rational choice. By the time drivers factor in battery value and limited repair networks, EV insurance becomes less about obligation and more about financial realism.

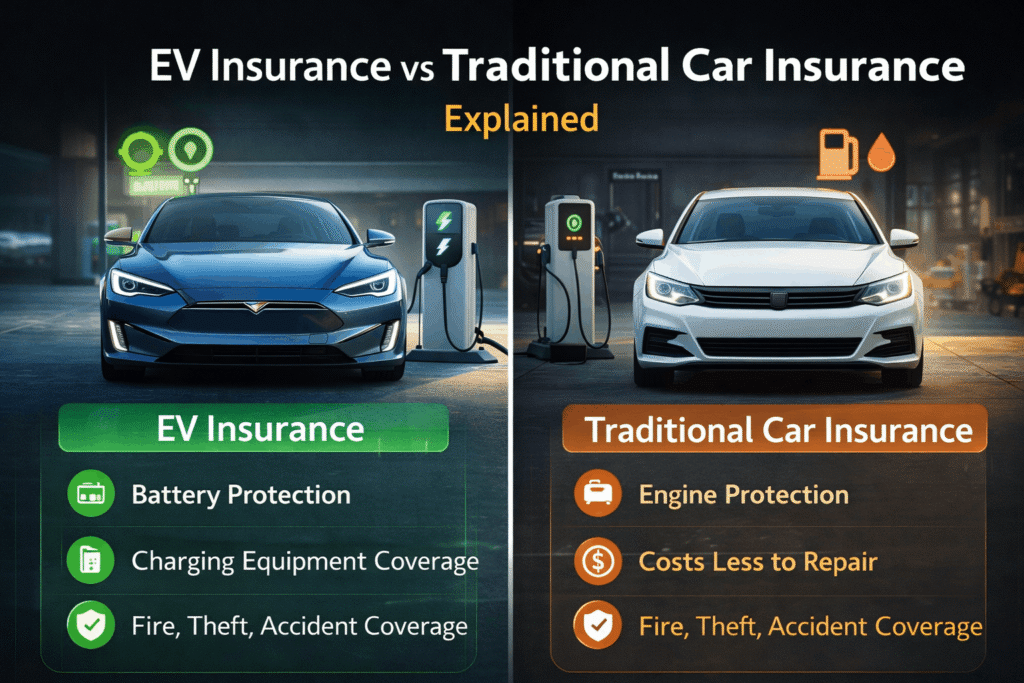

EV Insurance vs Traditional Car Insurance

EV insurance and traditional car insurance may share a familiar structure, but their priorities are fundamentally different. Internal combustion vehicles revolve around mechanical wear and fuel-related risks, while electric vehicles depend on electronics, software, and energy storage. That shift changes how insurers calculate exposure and protection.

Coverage differences emerge quickly when comparing policies side by side. EV-focused plans emphasize battery health, electrical safety, and charging infrastructure, areas that standard policies rarely address in depth. Cost comparisons can be surprising, as premiums may be higher upfront but often reflect fewer moving parts and lower long-term maintenance risks.

Risk assessment also diverges. Electric vehicles carry unique threats, from thermal runaway in batteries to limited availability of certified repair centers. These factors are built directly into electric vehicle insurance pricing models, rather than treated as anomalies. The result is coverage that feels purpose-built rather than adapted, reinforcing why electric vehicles demand their own insurance logic.

How Much Does EV Insurance Cost?

EV insurance pricing is driven by a blend of familiar and entirely new variables. While age, location, and driving history still matter, electric-specific factors weigh heavily in premium calculations. Insurers look closely at the components that are most expensive to repair or replace, especially when specialized labor is required.

Battery value plays a central role in cost determination. A larger or more advanced battery increases the insured value of the vehicle, which directly affects premiums. Repair costs further influence pricing, as EV-certified workshops and parts availability can vary widely by region. Brand and model also matter, with premium EVs often carrying higher insurance costs due to advanced technology and limited supply chains.

The affordability question depends on perspective. While electric vehicle insurance may appear expensive compared to entry-level petrol cars, it often balances out through fewer mechanical failures and lower long-term risk. As EV adoption grows and repair ecosystems mature, pricing is expected to stabilize, making coverage increasingly competitive rather than prohibitive.

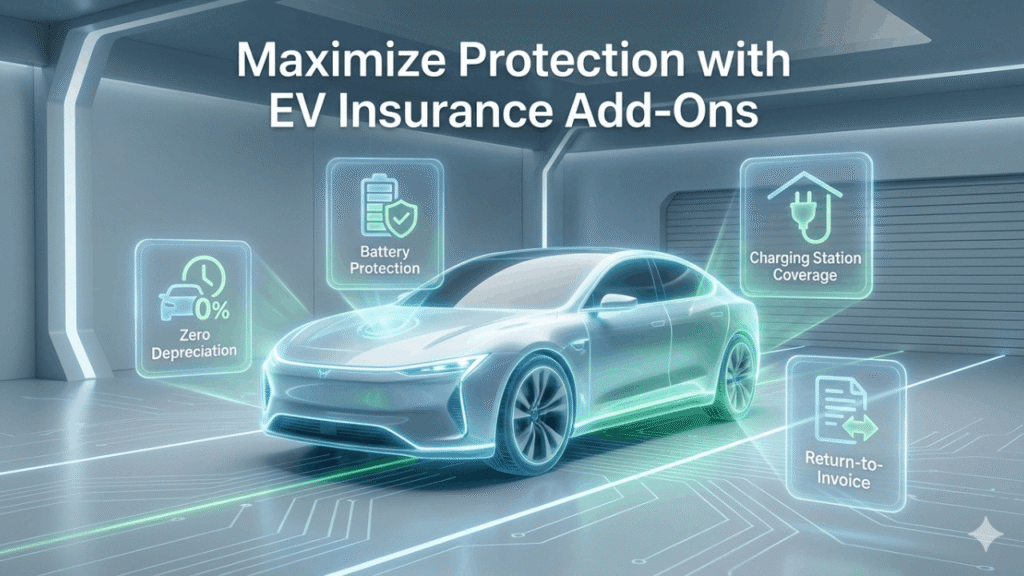

Best EV Insurance Add-Ons

EV insurance becomes significantly more powerful when paired with the right add-ons. These optional protections address gaps that standard coverage might overlook, especially in the early years of ownership when vehicle value is highest.

Battery protection add-on

This extension focuses exclusively on safeguarding the battery against degradation-related damage or unforeseen electrical failures not fully covered under base policies.

Zero depreciation cover

Electric vehicles lose value differently than conventional cars. Zero depreciation ensures that claim settlements under electric vehicle insurance reflect replacement costs rather than market depreciation.

Charging station coverage

Home charging equipment is a critical part of EV ownership. Some policies extend protection to wall-mounted chargers damaged by electrical surges or insured incidents.

Return to invoice (RTI)

RTI bridges the gap between insured value and purchase price, offering peace of mind during total loss scenarios early in ownership.

How to Choose the Best EV Insurance Policy

EV insurance selection demands more scrutiny than simply chasing the lowest premium. Buyers need to evaluate how well a policy understands electric vehicle realities, not just how cheaply it is priced. Coverage limits should align with battery replacement costs, not outdated valuation models.

Exclusions deserve particular attention. Some policies quietly limit battery claims or exclude charging-related incidents, which can undermine the purpose of specialized coverage. A strong claim settlement ratio is another critical signal, revealing how reliably an insurer honors commitments when things go wrong.

The best choice balances breadth of coverage with proven service quality. Electric vehicle insurance works best when it removes uncertainty, not when it adds fine print to an already complex ownership experience.

Best EV Insurance Providers

EV insurance providers separate themselves through expertise rather than branding alone. Leading insurers invest in EV-specific underwriting teams, partnerships with certified repair networks, and streamlined digital claims processes tailored to electric vehicles.

Reliability shows up in consistency. Providers that handle battery claims efficiently, offer transparent pricing, and adapt quickly to new EV models tend to outperform generic insurers. While market leaders vary by region, the most trusted names share a focus on data-driven risk assessment and customer education.

Choosing a provider with demonstrated electric vehicle experience reduces friction during claims and repairs. In a market still evolving, that reliability can matter more than marginal differences in premium pricing.

How to Buy EV Insurance Online

EV insurance purchasing has become a largely digital process, reflecting the tech-forward nature of electric vehicles themselves. Online platforms allow buyers to compare coverage options quickly, filtering plans designed specifically for EVs.

The process typically begins with entering vehicle details, including battery specifications and charging setup. Add-ons can then be selected based on usage patterns and risk tolerance. Payment completes the process, often followed by instant policy issuance.

This streamlined approach reduces paperwork and improves transparency. For EV owners accustomed to app-based vehicle management, buying electric vehicle insurance online feels like a natural extension of the ownership experience rather than an administrative chore.

Pros and Cons of EV Insurance

EV insurance brings a distinct mix of advantages and trade-offs that reflect the realities of electric mobility.

Pros

Specialized EV coverage ensures that batteries, motors, and charging systems are not treated as afterthoughts. Battery protection significantly reduces financial exposure, while long-term savings emerge through lower mechanical risk and fewer moving parts.

Cons

Premiums can be slightly higher, particularly for new or premium models. Limited repair workshops in some regions may also affect claim timelines, a challenge that electric vehicle insurance continues to adapt to as infrastructure expands.

FAQs About EV Insurance

Is EV insurance more expensive than regular car insurance?

EV insurance can appear slightly more expensive at first glance, mainly because electric vehicles have higher upfront values and costly battery systems. However, this difference narrows over time as EVs require fewer mechanical repairs and experience lower engine-related failures. Many insurers now price electric vehicle insurance competitively as repair data becomes more predictable. The long-term cost often balances out rather than remaining consistently higher.

Does EV insurance cover battery replacement?

Battery coverage is one of the defining features of EV insurance, but it is not unlimited. Most comprehensive policies cover battery damage caused by accidents, fire, or electrical faults, while gradual degradation is usually excluded. Some insurers offer dedicated battery protection add-ons that expand this coverage significantly. Understanding battery-related terms is critical before finalizing any electric vehicle insurance policy.

What happens if my EV runs out of charge on the road?

Running out of charge is treated differently from fuel depletion. Many EV insurance policies include EV-specific roadside assistance that covers towing to the nearest charging station. This service recognizes range anxiety as a legitimate risk rather than driver negligence. Without this feature, roadside support may be limited, making it an important detail to confirm.

Are home charging stations covered under EV insurance?

Home charging equipment is not automatically covered under all electric vehicle insurance plans. Some insurers include wall-mounted chargers under add-on protection or as part of comprehensive coverage when damage occurs due to insured events. Electrical surges, fire, or vandalism may qualify, depending on policy wording. Owners relying heavily on home charging should verify this inclusion explicitly.

Can I transfer EV insurance when selling my electric vehicle?

Yes, EV insurance is generally transferable to the new owner, following standard vehicle insurance transfer procedures. The insurer may reassess risk based on the buyer’s profile, which can affect premium adjustments. Battery condition and vehicle age also influence transfer approval. Timely documentation ensures continuity of coverage without policy lapses.

Does EV insurance cover software-related issues?

Most EV insurance policies do not cover software glitches unless they result in physical damage caused by an insured event. Software updates, system bugs, or manufacturer recalls typically fall outside insurance scope. However, damage caused indirectly by software failure may still be considered under comprehensive electric vehicle insurance. This gray area makes manufacturer warranties equally important.

Conclusion: Is EV Insurance Worth It?

EV insurance reflects the broader shift toward electric mobility, offering protection that aligns with modern vehicle design rather than outdated assumptions. Its value lies in understanding where risks truly exist and addressing them with precision.

For drivers committed to electric vehicles, specialized coverage is not just worth considering, it is increasingly essential. Choosing the right policy ensures that innovation on the road is matched by confidence off it.

3 thoughts on “EV Insurance Explained: Protect Your Electric Vehicle Like a Pro in 2025”

Comments are closed.